Due Diligence

What is a Due Diligence clause and do I need one?

Learn what a Due Diligence clause is, how to use it, and what it means for you.

Property Investment

11 min read

Author: Ed McKnight

Our Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Reviewed by: Laine Moger

Journalist and Property Educator with six years of experience, holds a Bachelor of Communication (Honours) from Massey University.

If you’ve been considering investing in property for a while – you might be wondering: “How do I actually plan out a property portfolio?”

That’s a great question and one most property investors start out asking. That’s because there’s a lot to decide.

You’ve got to figure out what to buy and when to buy. You’ve also got to calculate how much you have to spend.

So, this article is going to “pull back the curtain” and show you:

The first two principles are based on building a diverse portfolio.

I get that sounds boring … so let’s put it a different way.

You want to add properties to your portfolio that complement one another.

This is often called a wealth wheel. What’s a wealth wheel?

It’s where you might buy a few properties that have poor cashflow and then complement it with properties that have good cashflow.

Here’s an example. Let’s say you buy a property that has great capital growth potential. But, over the long term, it might lose $50 a week once interest rates rise.

This sounds manageable, so you buy another one.

You’ve now got 2 investment properties that you expect will increase in value. And they cost $100 a week in total to hold.

You then decide you want to buy a few more. But you can’t afford to keep putting in an extra $50 a week per property. Or, maybe the prospect of keeping on buying negatively geared properties sounds a bit risky.

That’s when you might purchase a high yielding property – like a dual-key apartment – which might earn $150 a week in cashflow.

You take that cashflow and use it to pay for your other two properties.

So the apartment earns $150 a week. The two growth properties require a $100 a week top-up. That leaves $50 leftover.

You can then use that to subsidise the purchase of another growth property.

In this wealth wheel, you bought 2 growth properties and then a yield. That’s what we call GGY. Because your wealth wheel is 2 growth and a yield.

As you're building your wealth wheel, you can keep this little acronym in mind, so you know what you’re due to buy next.

For instance, if your plan is to buy 3 growth properties before adding a yield property, your acronym would be GGGY.

If you can get your properties to complement one another in this way, you’re more likely able to hold them for the long term. That’s because the cashflow supports one another.

In simple terms – properties that work together – stay together.

The second fundamental principle is – to use a cliché – don’t put all your eggs in one basket.

To put that in property investment terms, you don’t want to put all your properties in the same housing market.

Why’s that? Well, property prices go up, sometimes they come down. And for long periods, they’ll stay the same.

But here in New Zealand, each region’s property market tends to operate independently.

That means that property prices in Auckland can be skyrocketing while Wellington is flat. In other times, Wellington will be booming while Auckland prices are going backwards.

Take a look at this graph –

Auckland prices increased 86% between January 2010 and mid-2015. Over that same timeframe, Wellington was up only 6%.

But then what happened between September 2016 and April 2020?

Auckland was up 6%, whereas Wellington house prices were up 43%.

What’s the message? It’s not to buy in either Wellington or Auckland. But instead to invest in multiple property markets, so it’s more likely that you’ll have at least one property in a booming market.

One of the big questions early-stage investors ask is – “after I buy my first investment property … when will I be able to buy the next one?”

At some point, investors tend to get tapped out of equity in the early part of their investing life.

They’ve bought properties and now don’t have the deposit to go and purchase another one.

If you’re following a passive buy and hold strategy – focussed on New Builds – then the two main ways to increase your equity are:

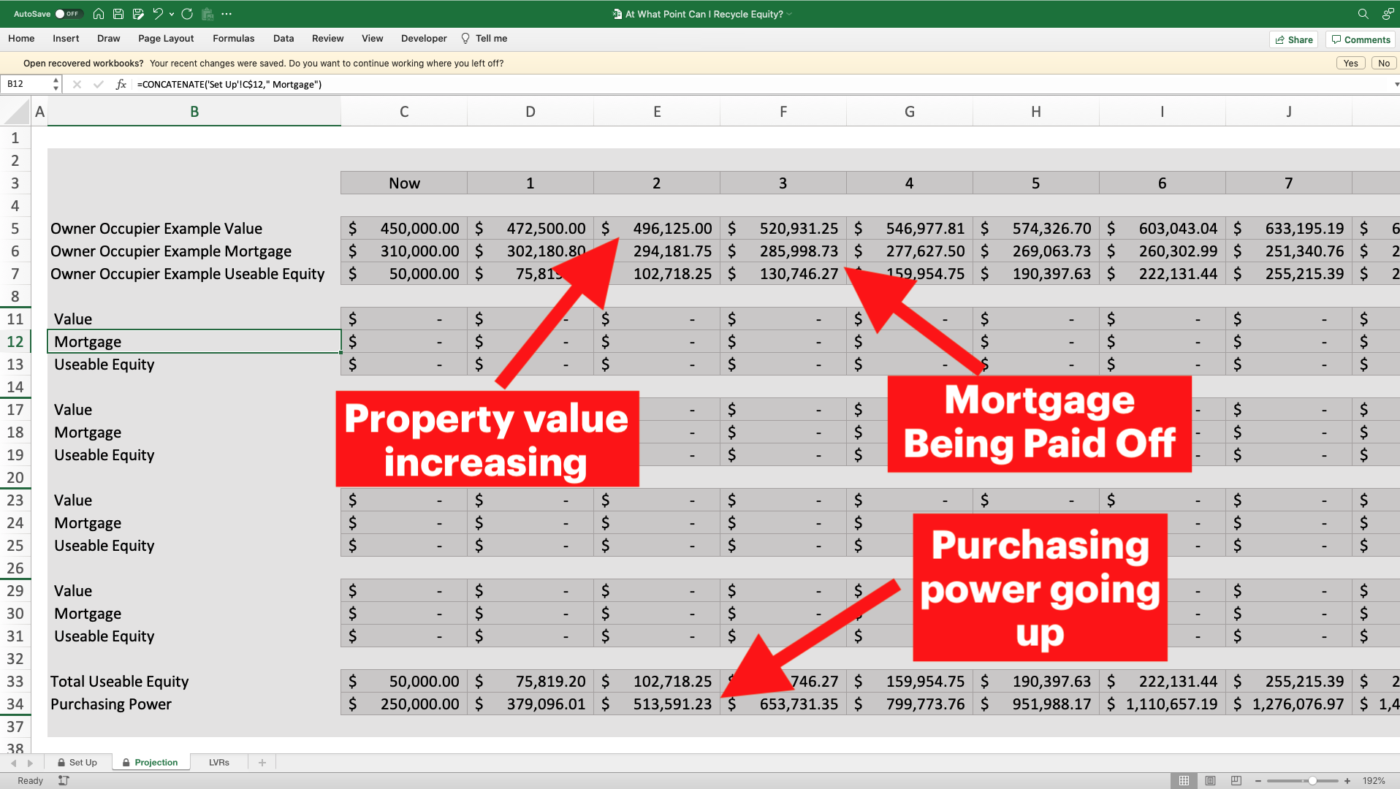

This is where you can use a spreadsheet like the below to project when you might have the equity to purchase another property.

You can then also test whether paying down debt more rapidly will help you grow your portfolio sooner. Download the spreadsheet here.

Ok, let’s now get into a case study of how a couple might plan out a portfolio and how the portfolio might meet their long term goals.

Our example couple is Bill and Jean. They live in Wellington and are aged 47 and 48, respectively. They’re happily working and plan to retire in 20 years. They want to build a passive income in retirement to supplement their savings.

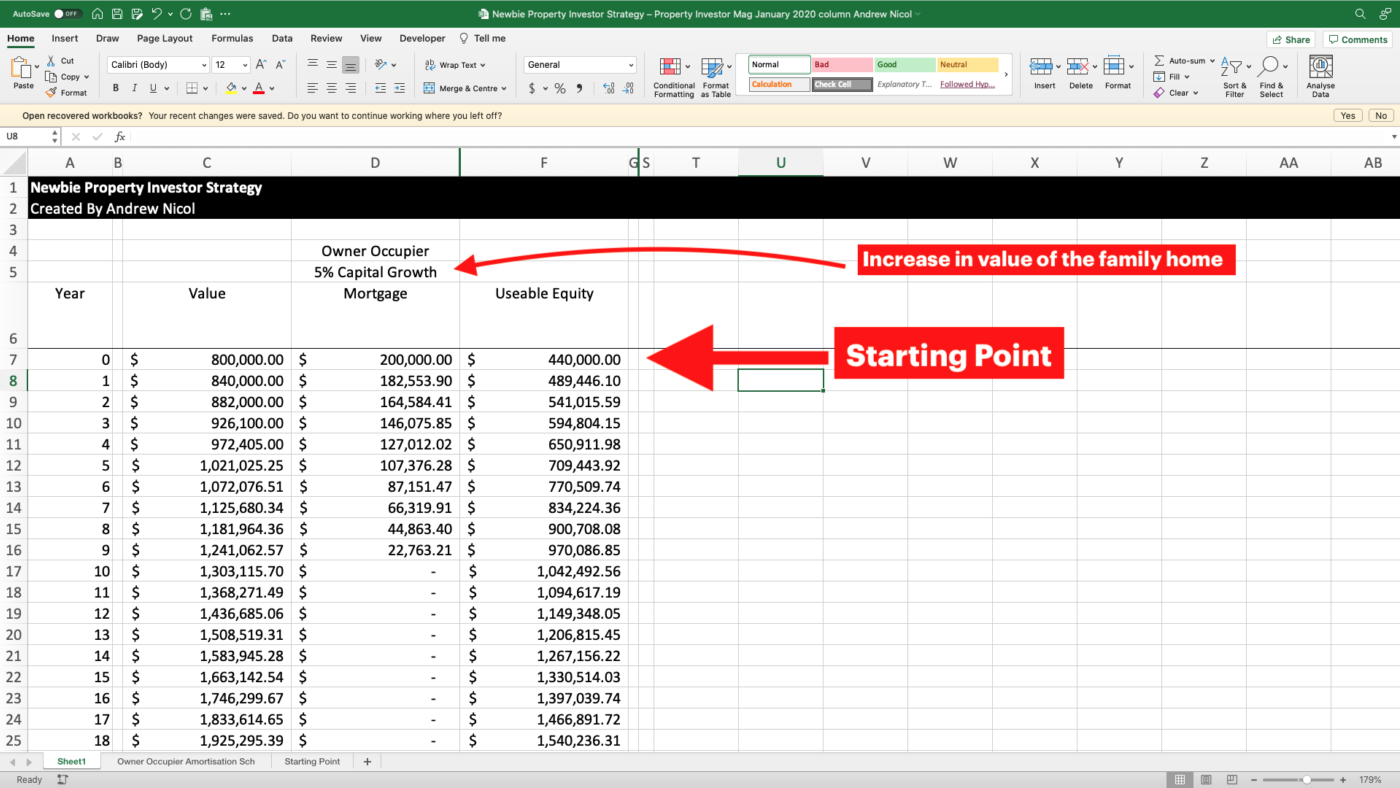

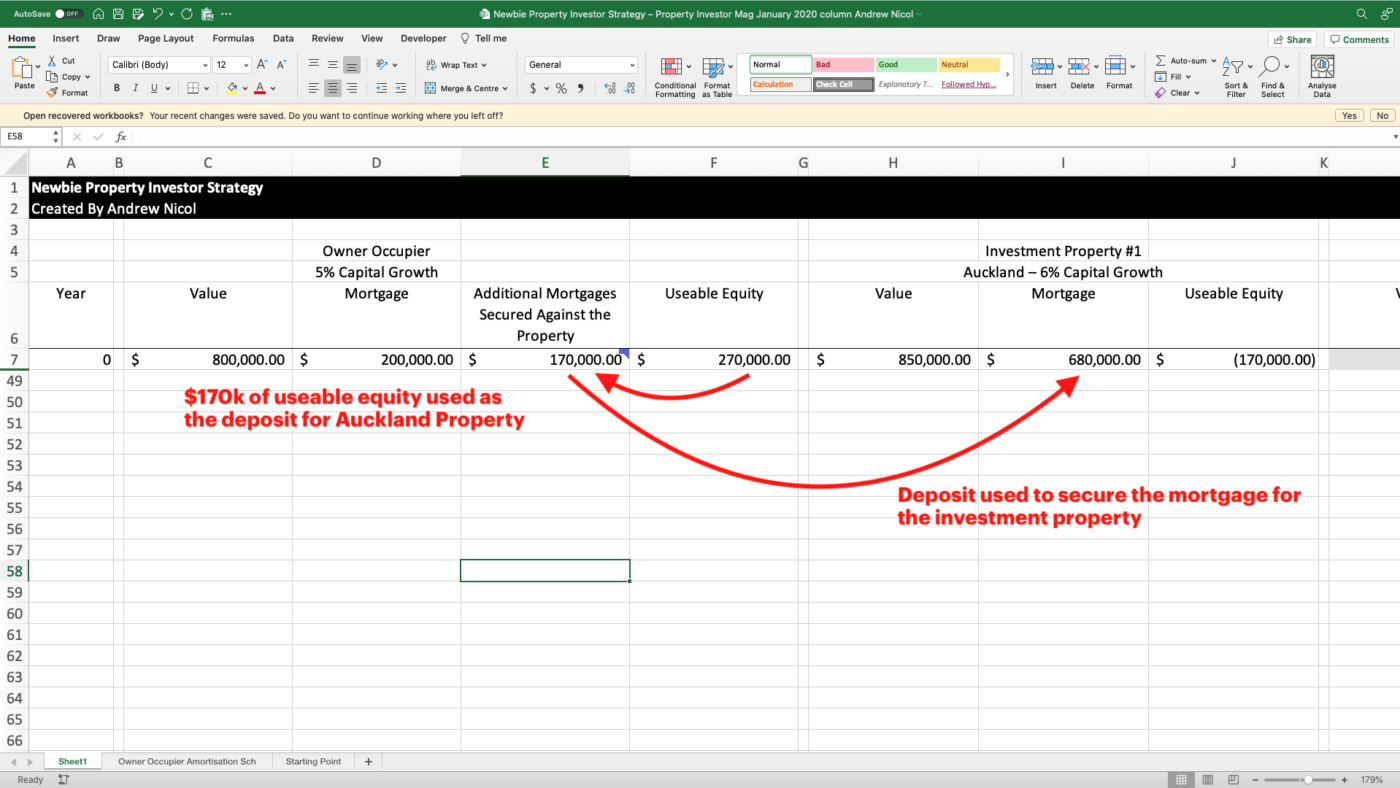

They are in a healthy equity position. The couple’s family home is worth $800,000. And since they’ve been paying down their mortgage over time, they’ve only got $200,000 left to pay over the next ten years.

These numbers mean that Bill and Jean could purchase up to $2.2 million worth of New Build properties without having to touch their savings.

Now that we have a goal (build passive income), the resources to achieve that goal (equity in the home) and a time horizon (20 years), we can create a portfolio.

Here’s what Bill and Jean might look to do:

It is usually best to begin your portfolio by investing in properties that will likely achieve good capital growth.

These properties may require the investor to ‘top-up’ the mortgage each week (i.e. be negatively geared), but they will increase in value more quickly.

You would typically start with these capital growth properties for two reasons:

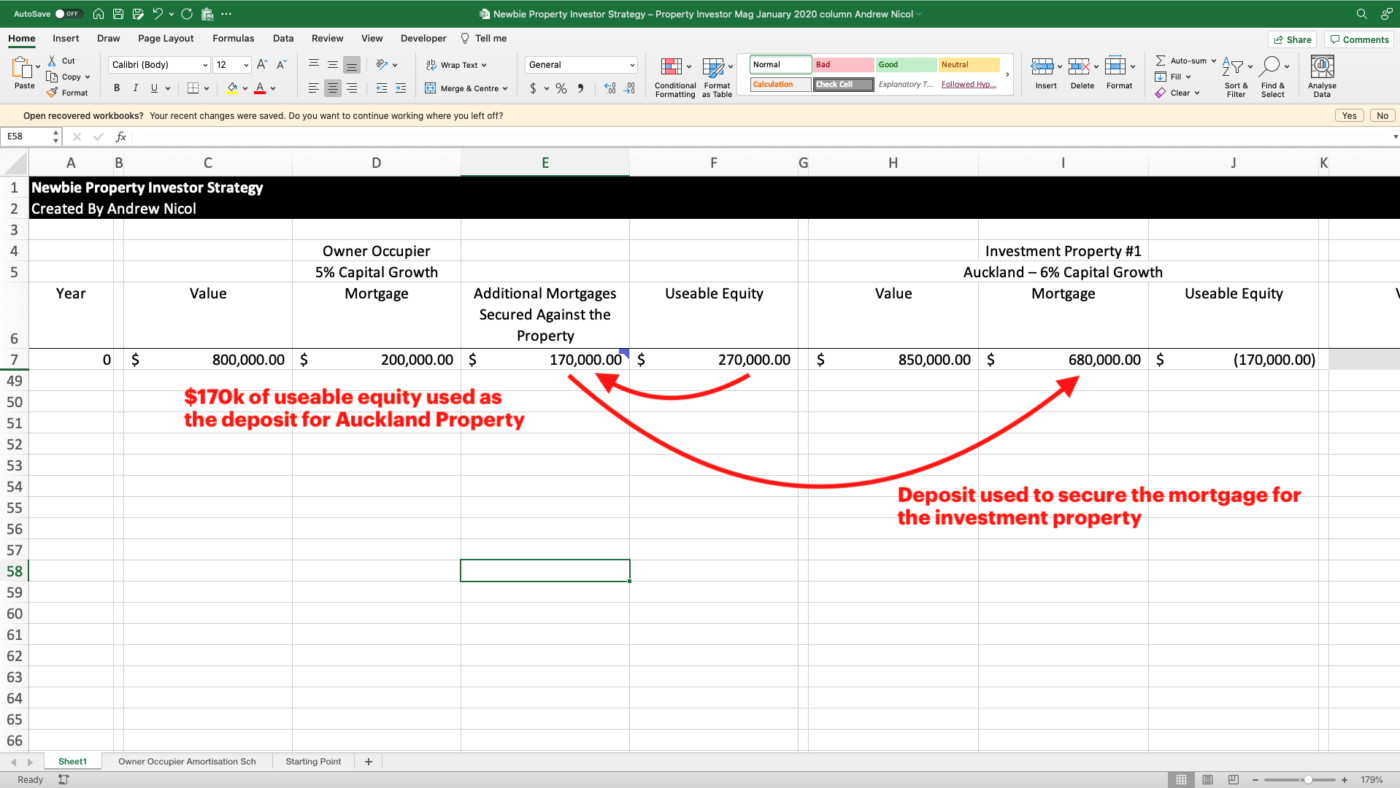

Let's look at a basic portfolio strategy:

At this point, the couple has $370,000 of mortgages secured against their home. That’s because the $170,000 deposit for the investment property is tagged against their own equity.

At this point, the couple will still have the ability to purchase another $1.35 million of investment properties.

They have the equity to purchase another property straight away. However:

So the couple might wait, and then over the next few years, they might:

Let’s assume the Hamilton property will also be negatively geared and also requires a top-up of $50 a week. So the portfolio will need a $100 a week top-up across both the Hamilton and the Auckland property.

Because the Wellington property earns $125 a week, it can pay $100 top-up for the other properties. That means that the portfolio is no longer negatively geared.

So, at this stage, there is $440,000 worth of investment debt secured against their home. However, the rent from the investment properties will cover these interest payments.

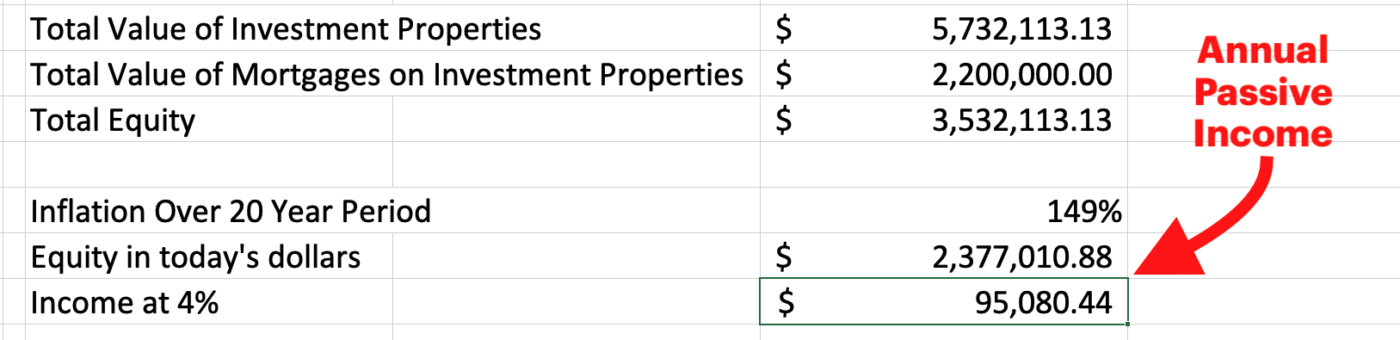

By investing in high yielding property, Bill and Jean’s wealth would increase as the properties slowly rise in value. This ‘inflation-proofs’ their retirement strategy, making them set for life.

Our Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

Ed, our Resident Economist, is equipped with a GradDipEcon, a GradCertStratMgmt, BMus, and over five years of experience as Opes Partners' economist. His expertise in economics has led him to contribute articles to reputable publications like NZ Property Investor, Informed Investor, OneRoof, Stuff, and Business Desk. You might have also seen him share his insights on television programs such as The Project and Breakfast.