Property Investment

What should my retirement plan look like?

Thinking about retirement? The Epic Guide to Retirement Planning is the guide that will give you the knowledge so you can plan for your retirement in 2026

Wealth

15 min read

Author: Andrew Nicol

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Reviewed by: Ed McKnight

Resident Economist, with a GradDipEcon and over five years at Opes Partners, is a trusted contributor to NZ Property Investor, Informed Investor, Stuff, Business Desk, and OneRoof.

One of the questions I get all the time here at Opes Partners is, “OK, Andrew, be honest: how much do I need to retire in New Zealand?”

And if you’ve been thinking about retirement, you’ll probably know there is a huge range.

Some people want to spend more in retirement. Others are happy to live a more modest lifestyle.

It also depends on where you live. It costs more to live in a city compared to a small town.

So you might be saying, “How much do I need to retire in NZ? Can anyone just help me answer this question and give me a solid budget?”

That’s why in this article you’ll learn:

And, by the end, you’ll have a great sense of what your retirement may look like.

There are 5 big decisions you need to make when you plan your retirement spending. These impact how much your retirement costs.

In other words, these 5 factors impact how much money you need in the bank to retire the way you want:

The more you want to spend, the more money you need in the bank when you retire.

Here are the 6 main lifestyles I discuss with investors:

The things you buy get more expensive over time. That’s inflation.

The New Zealand Society of Actuaries reports that older people tend to buy fewer things as they age.

You might spend more when you’re 65 and less when you are 90.

So your spending might not need to keep up with inflation.

If you’re happy buying fewer things as you age, then you don’t need as much money in the bank when you retire. As you get older the NZ Super will make up more of your income.

If you want to inflation-proof your spending, you’ll need more savings in the bank.

It’s morbid, but the longer you live, the longer you’ll be retired, so you need more money in the bank to fund those extra years.

If you think you’ll live longer, then you need more money. If you think you’ll pass away sooner, then you won’t need as much money.

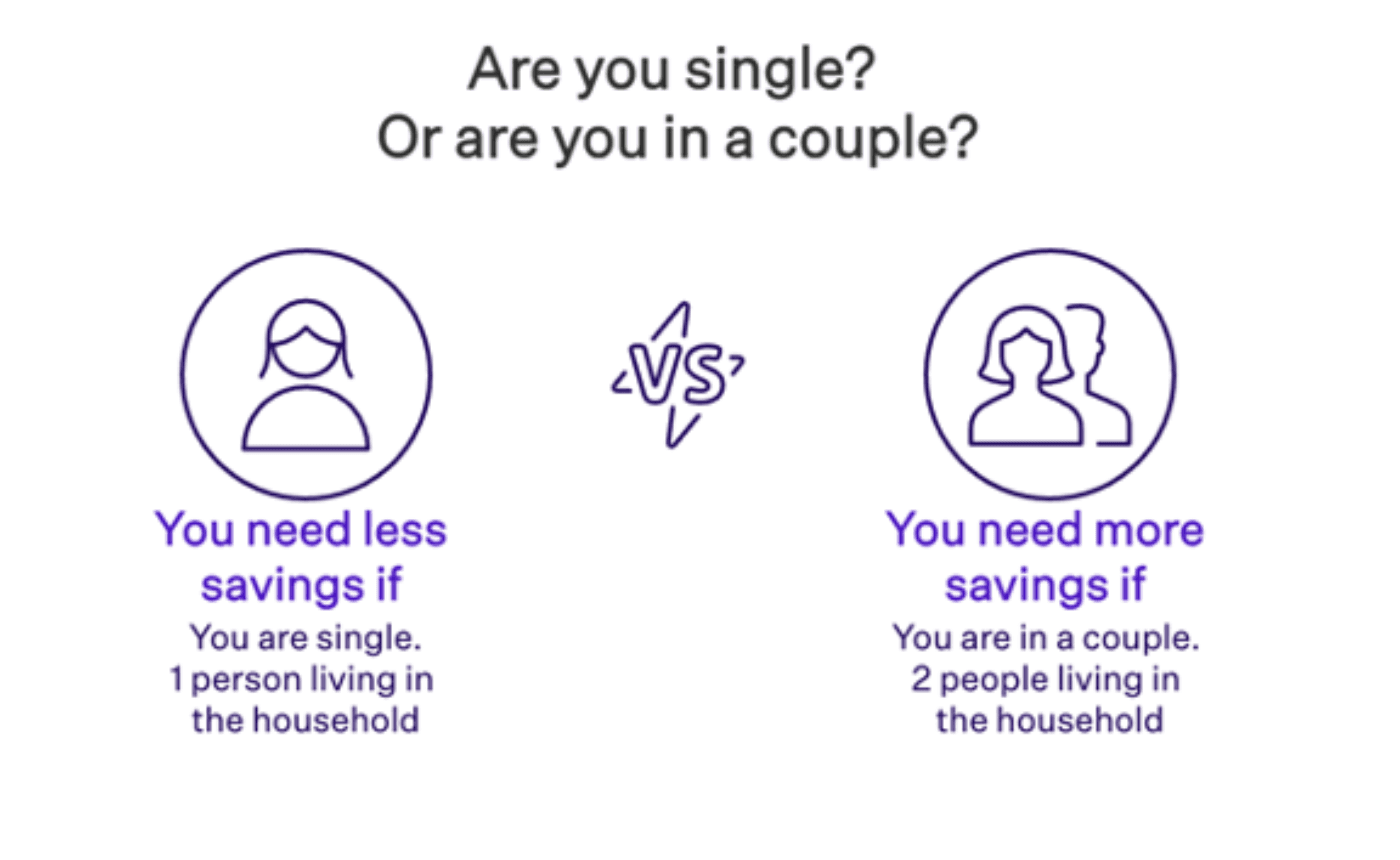

If you’re in a relationship, you generally need more money in the bank. That’s because you have 2 people to feed and house – rather than just 1.

Having said that, couples get more in NZ Super than a single person living alone.

And then you share your housing costs across 2 people, instead of just 1.

So couples usually need less in the bank (per person) but need more money overall.

Some investors want to live off the returns of their wealth and never touch their original nest egg. That means they can create generational wealth and pass on their money to family.

Other people don’t care about this. They want to die with $0 in the bank – having enjoyed it all.

If you want to preserve the value of your nest egg, you need more money because you just want to live off the returns.

If you don’t care about this (you’re happy passing away with $0 in the bank) then you don’t need as much in the bank.

There are lots of other factors that make your retirement more or less expensive.

For instance, if you think inflation will be lower, you need less money in the bank.

If you think inflation will be higher, you need more money in the bank.

If you think you can get a higher return, you need less money in the bank.

If you think your returns will be smaller, you need more money in the bank.

Here’s why we’re talking about these 5 decisions. The amount you, personally, need depends on how you set up your money.

You can retire with less money in the bank if you’re:

And that’s fine. Those are your decisions.

But you will need more money in the bank to retire if you’re:

Ultimately, only you (and your financial adviser) can say how much you need in the bank to retire well. An article on the internet (i.e. this article) can’t do that.

You might also want to get a feel for how much you might spend in retirement and what life looks like based on what you spend.

Here are the 6 lifestyles we often talk about at Opes Partners:

Spending: $40,000 / year as a couple

If you just want to live off the government pension, you can spend about $40,000 a year as a couple.

That’s what gets paid into your bank account.

Your budget will be very limited. According to Massey University research, you can spend about $17 a week on fruit and vegetables for two people.

If you are a single person, you don’t get as much. You’ll get around $24,000 a year to spend.

Most retirees spend more than what they receive from the government.

Although some people – especially older people – don’t spend much. They find they are quite happy just living off NZ Super.

If you just live off NZ Super you don’t need any savings in your bank account; the government is looking after you.

Spending: $47,500 / year as a couple

For a couple living a no-frills lifestyle, you could expect to spend just under $50,000 a year.

This budget covers the basics but leaves little room for extras, so you still need to be careful with your money.

At this level you’re spending less than the average retiree. In fact, over 60% of Kiwi couples aged 65 and over spend more than this each year. That’s if they live in a city.

At this point NZ Superannuation won’t cover all these costs, so you’ll need to save or invest to make up the difference.

This budget is also based on you owning your own home without a mortgage.

On the low end you might need as little as $20k in the bank to cover the difference. But, depending on how you set up your money life, you might need up to $206k.

Spending: $90,000 / year as a couple

Next, you have the Choices lifestyle.

Provided you have your own home and no mortgage, you should have a comfortable time. You can spend slightly more than the average retiree.

You have more choices and can afford the odd holiday around New Zealand.

You will need extra money for large purchases. e.g. buying a campervan. And if you have any health troubles, you’ll need to go through the public health system.

Like most of the other lifestyles, the NZ Super doesn’t cover it, so you’ll need some extra money to top up the pension

On the low end you might need as little as $630k in the bank to cover the difference but, a more mid-range estimate is $995k at the point you turn 65.

I’ll explain more about how these are calculated below.

Spending: $100,000 / year as a couple

This level of income starts to give you many more choices.

The home you live in; the holidays you take.

You can even take many more overseas holidays if you manage your money well.

If you are used to living on a high income while you’re working, this can allow you to continue your current lifestyle.

This is the lifestyle most investors I work with here at Opes Partners aim for.

If you pull a couple of the levers (mentioned above) to make retirement cheaper, you might need as little as $795k to fund this lifestyle. That’s as a couple.

At the mid-range you might need $1.2 million. Though, depending how you set up your life (and the choices you make), you might need up to $2.2 million.

Spending: $150,000 / year as a couple

Once you move into the affluent lifestyle, you can enjoy a very high quality of life.

You can drive the car you want and you can upgrade your car every few years.

You can travel where you want.

You have choices and can easily handle health concerns; you can pay for treatment if needed.

If you want to go through a private hospital, you can do that. You don’t have to wait for a doctor through the public system.

But you also need a lot more money in the bank to fund this type of lifestyle.

On the low end you might need as little as $1.6 million in the bank to cover the difference. But, the mid-range estimate is $2.2 million.

That’s a lot of money!

But, the reason it’s high is because people living this lifestyle want to spend a lot each year. And they want to do it for 25 years+ without going to work.

To see how this is calculated, read more below.

Once you move to the Contribution lifestyle, you are in the top couple of %.

Not many people spend this much in retirement. That’s because you need to be very rich to sustain this level of spending.

But if you can, it’s a very, very high-quality lifestyle, and you can support others.

You can help the kids and grandchildren. You can donate to charities important to you.

Brace yourself, because the numbers are big!

To spend this level of money you need at least $2.45 million in the bank (on the low end). The mid-range estimate is $3.3 million. That’s to top up your NZ Super.

For each of the 6 lifestyles, we’ve given 3 options for the amount of money you might need – low, mid and high.

And you might be thinking: “How are these actually calculated?”

Here are the main differences:

In the low scenario, this is the amount of money you’d need if:

You also plan that your real spending will decline over time.

So every year, your spending doesn’t quite keep up with inflation, so you buy fewer things.

You might start by spending the equivalent of $100,000 in today’s money (while you’re 65).

Then, by the time you are 90, you spend the equivalent of $60,000 a year (in today’s money).

According to the NZ Society of Actuaries, many retirees decrease their spending over time.

That means the NZ Super becomes a more important part of your income over time and you use less and less of your savings.

In the mid scenario, you’re still 65, planning to run out of savings at 90, but this time your real spending doesn’t decrease over time.

You increase your spending each year to keep up with inflation. That means you can continue to live the same type of lifestyle throughout retirement. You don’t have to pull back.

This is a standard assumption that many financial advisers use.

You will also likely change what you spend money on throughout retirement.

You might start spending more on holidays. Then, as you age, spend more on healthcare and the cost of a retirement village.

In the high scenarios, you are still retiring at 65, but this time you live off the returns of your investments. You don’t spend any of your savings.

That means that your money ‘doesn’t run out’. You can live well past 90 and you still have money available.

Then you can pass your assets on as generational wealth.

Here at Opes Partners (the website you’re on), we’re a property investment company. So often investors set this up by buying high income properties with very low mortgages.

Then they live off the rental income.

Because property and rental income tends to go up over time, this helps to protect your wealth against inflation.

As you choose your lifestyle, you need to balance what you want with what’s achievable.

You might think, “Of course, I want to spend $200,000 a year.”

But if you have a big goal, you need to save and invest more today.

To invest more, you need to spend less today, so there is a trade-off.

A big lifestyle in the future could mean cutting back more today.

But the flip side is true, too.

If you spend all your money today (and don’t invest), you’ll have fewer choices in the future.

So, you need to balance what you want with how much you’re willing to invest.

Just keep in mind that the bulk of retirees spend more than superannuation.

So, paying off the mortgage and living on the pension is not enough for most people.

Although there are 20-30% of New Zealanders who survive just on the pension.

Here are a few case studies to show you the sort of lifestyles Kiwis are aiming for.

I first met Tanya when setting up Opes Partners back in 2013. She already had two investment properties which she had owned for a decade each.

She was 57 at the time with two teenage sons. She wanted to build a passive income and didn’t want to rely on the government pension.

Over the next few years I helped her buy 2 more investment properties.

In 2021, Tanya sold her 4 properties and bought 2 high-income apartments without a mortgage.

Together, these rental properties earn her $1,500 a week before tax. Then, she gets the NZ Superannuation.

Once you factor that in, Tanya can spend $82,200 a year. That continues whether she lives to 82, 92 or 102.

Tanya is living the Choices lifestyle, and she has chosen the high scenario. Her spending doesn’t reduce as she ages and she has assets to pass on to her sons.

Bruce and Carol took a different approach. When I met Bruce, he was 49, and Carol was 46.

We worked out that if they invested in 3 properties over the next 7 years, they could spend $57,000 a year in retirement. They would then have their superannuation, too.

By the time Bruce hit 65, the value of their properties had gone up and they’d paid off a bit of debt.

So, they sold one of their properties and kept $57,000 in their account. That’s what they wanted to spend that year. They then invested the rest in a term deposit.

Every year, they’ll take another $57k out to spend and then reinvest the rest.

When they need more money, they’ll sell another one of their properties.

Bruce and Carol can spend $96,709 a year. That means they are close to the Well-off lifestyle. And they have chosen the mid-scenario. They’ll eventually run out of savings.

But that’s OK. They’ll still have the family home to pass on to their children. And it means they can spend more in their retirement (compared with just living off the returns).

I get it. These numbers are big. So you might be thinking … “How do I build up that level of assets?”

Well, there are two options:

Either pull some of the levers (discussed above) and make your retirement cheaper.

Or, you can invest more to get to the level of wealth you want.

One option many Kiwis consider is investing in property. If you’re in the same boat you might like to come to see us at Opes Partners, just like Tanya, Bruce and Carol.

We can create a free retirement plan using our in-house software, MyWealth Plan. That way you’ll know how many properties you need to invest in. We can then help you find the properties that suit your retirement plan.

Managing Director, 20+ Years' Experience Investing In Property, Author & Host

Andrew Nicol, Managing Director at Opes Partners, is a seasoned financial adviser and property investment expert with 20+ years of experience. With 40 investment properties, he hosts the Property Academy Podcast, co-authored 'Wealth Plan' with Ed Mcknight, and has helped 1,894 Kiwis achieve financial security through property investment.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser